- Download LiquidPay from the App Store or Google Play.

- Register and verify your identity using Singpass.

- Link a credit card inside the app.

- At the stall, open LiquidPay and scan the NETS QR code. It works at NETS QR terminals that accept LiquidPay — look for the LiquidPay or XNAP logo.

- Enter the amount, confirm, and the stall gets paid.

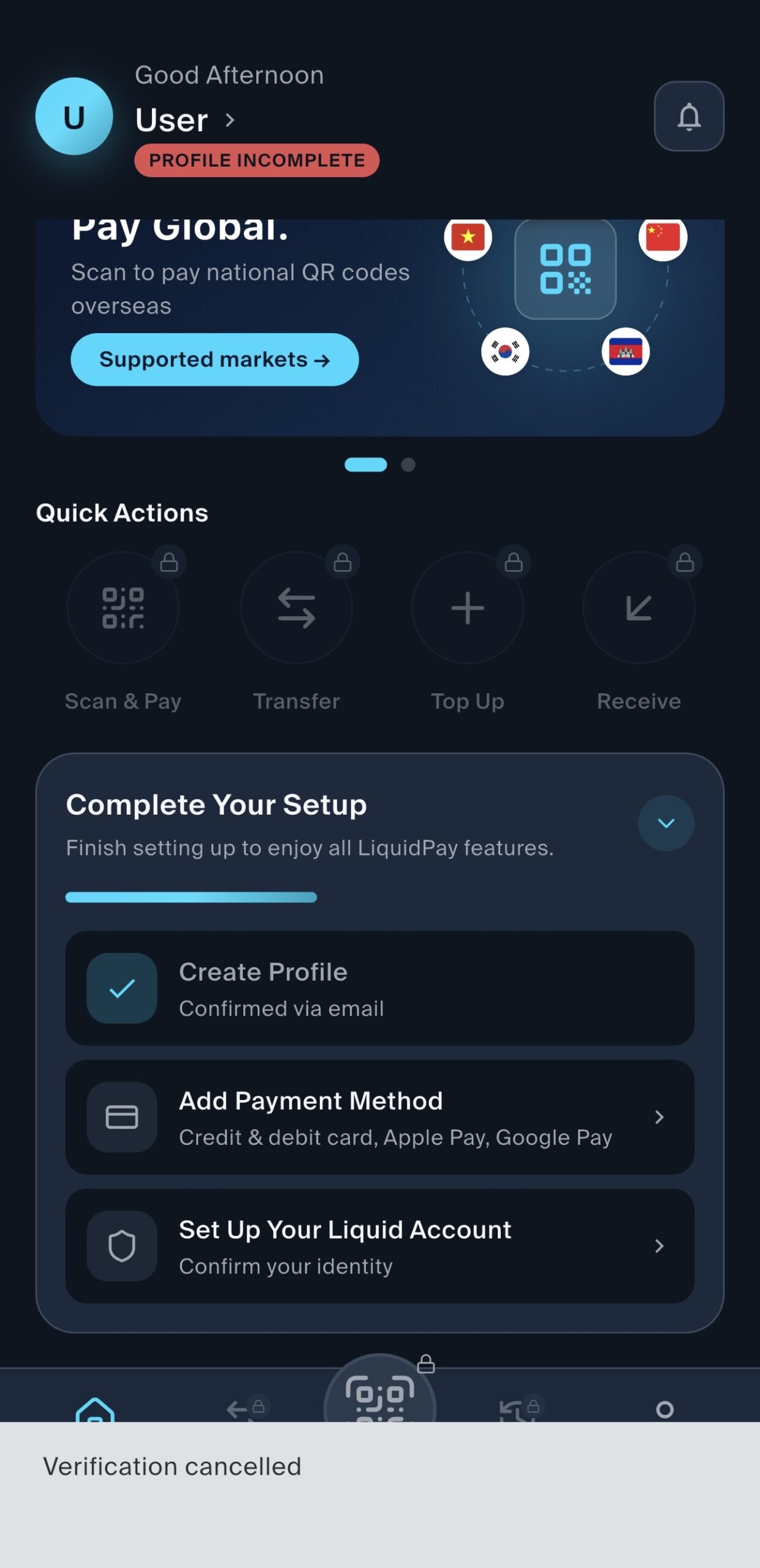

Setting up LiquidPay in-app. Singpass identity verification can take hours — mine took about 5 — and may show “Verification cancelled” before it completes.

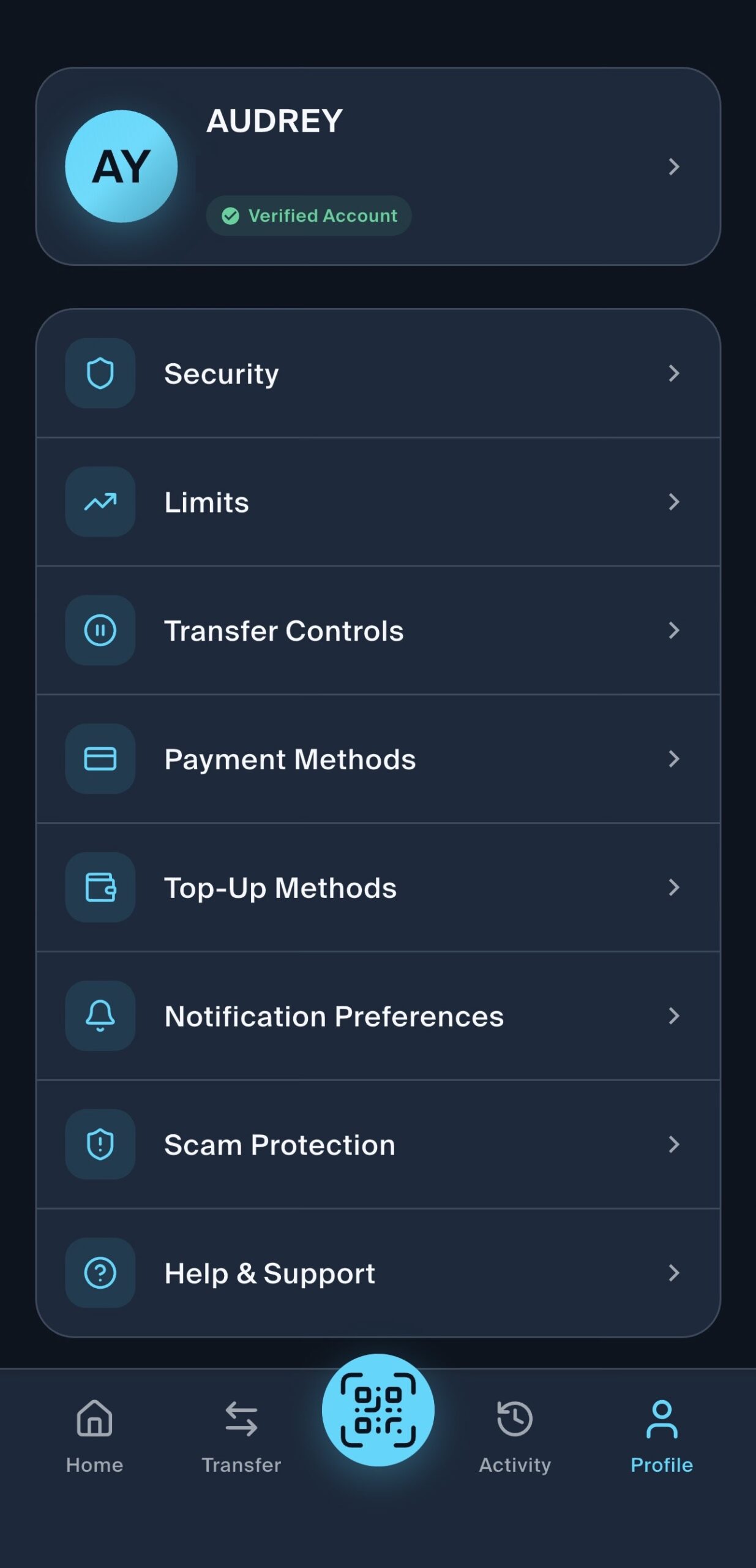

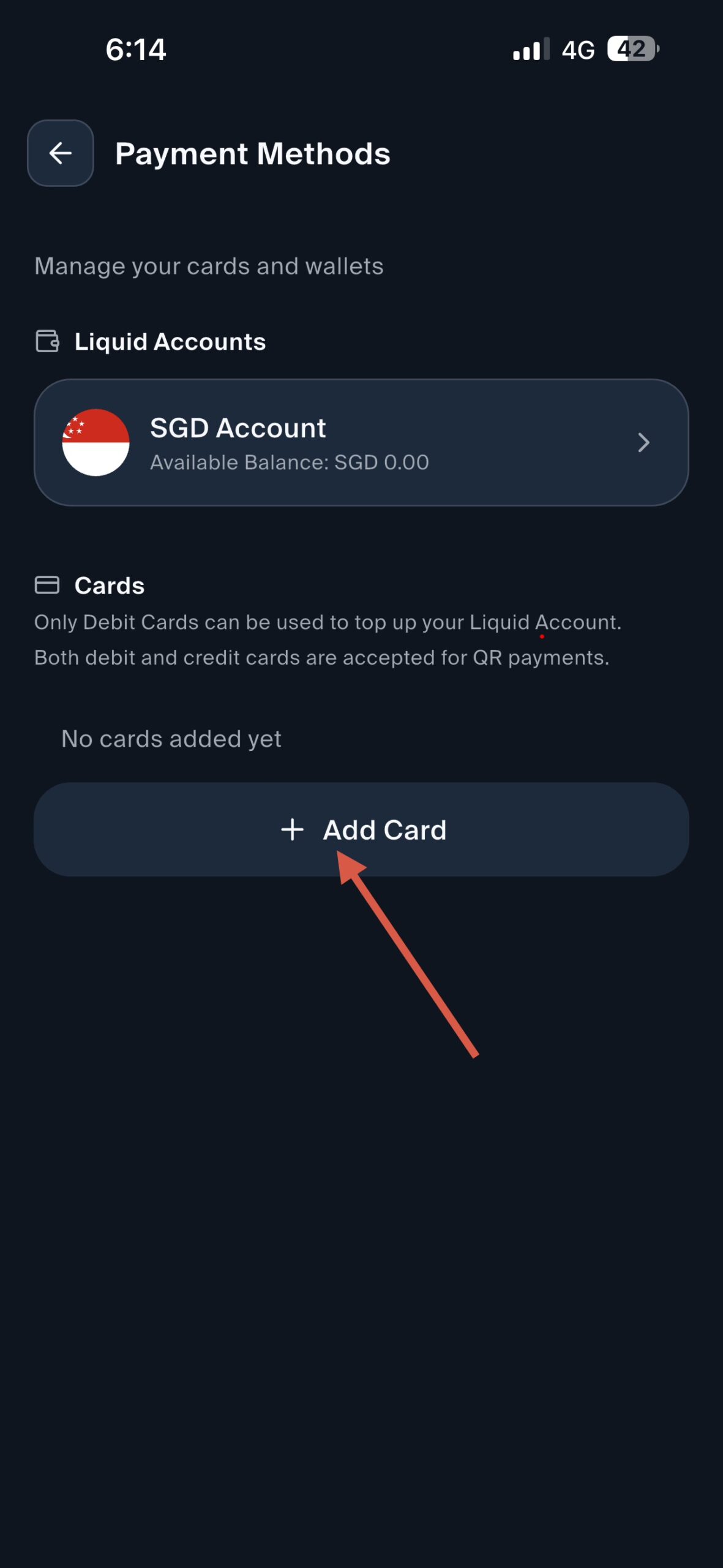

Step 1 — from your Profile, tap Payment Methods.

Step 2 — tap Add Card. Note the app’s own line: only debit cards can top up your wallet, but both debit and credit cards work for QR payments.

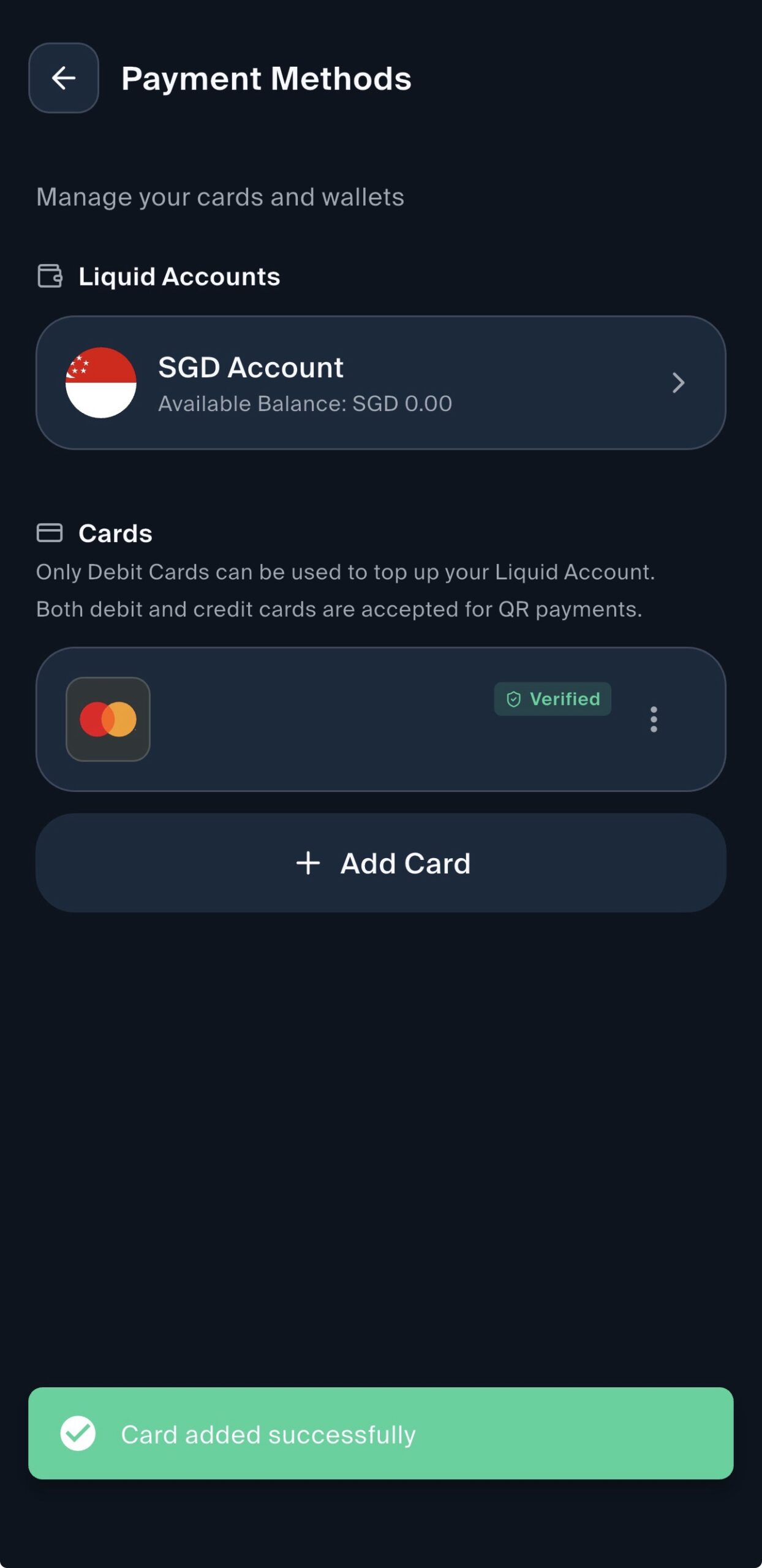

Step 3 — your credit card shows as Verified once added.

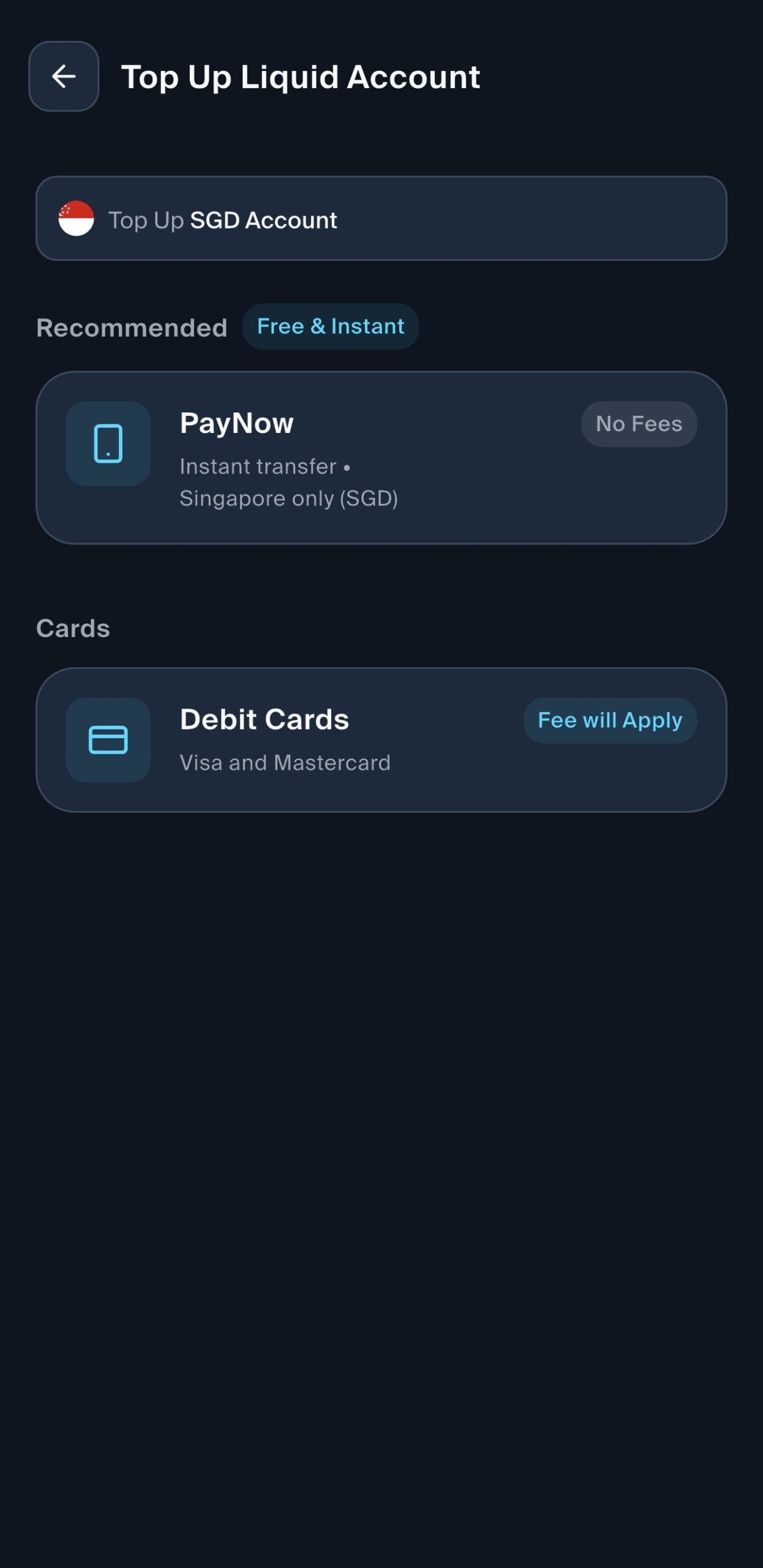

Skip the Top-Up screen — it only takes PayNow or a debit card (with a fee). You do not need to top up; the linked card charges your credit card directly.

| Card | Type | Earn rate | Cap & min spend |

|---|---|---|---|

HSBC Revolution HSBC RevolutionApply | Miles | 4 mpd (8 mpd with S$50K EGA balance) | S$1,000 / calendar month · no min spend |

Citi Rewards Citi RewardsApply | Miles | 4 mpd | S$1,000 / statement month · no min spend |

DBS Woman’s World DBS Woman’s WorldApply | Miles | 4 mpd | S$1,000 / calendar month · no min spend |

UOB Preferred Visa UOB Preferred VisaApply | Miles | 4 mpd | S$600 / calendar month (online category) |

UOB EVOL UOB EVOLApply | Cashback | 10% (online & mobile contactless) | S$30 / month cap · S$800 min spend |

Maybank Family & Friends Maybank Family & FriendsApply | Cashback | 8% under the Online Shopping category (6% at lower tier) | S$1,600 min for 8% (S$800 for 6%) |

| OCBC FRANK | Cashback | Up to 8% | S$25 / month |

| DCS Flex | Cashback | Up to 6% | S$25 / month |

ENDS 16 AUG 2026 · 7 DAYS LEFT

🎁 Choose 1 Gift

Selection form emailed after application

Dyson Airstrait™ Straightener

Retail S$799

Hair straightener that dries and smooths hair at the same time

25,000 Max Miles by Heymax

Worth S$600+

Earns you miles redeemable for flights, hotels, and perks

Dyson V8 Cyclone Vacuum Cleaner

Worth S$559

Cordless cleaning vacuum with strong suction

Sony WF-1000XM6 (Earbuds) + S$50 eCapitaVoucher Bundle

Worth S$529

Amazing earbuds and voucher bundle

S$461 Cash

Worth S$461

via PayNow

Valid till 16 Aug 2026

Requirements

- You qualify if: you have no HSBC credit card right now, AND haven't cancelled any HSBC credit card in the last 12 months

- Spend min. S$500 by the end of the month after you're approved. Example: approved in May → spend by 30 June.

- During the application, tick the box to receive marketing messages from HSBC. Don't unsubscribe until your gift arrives — if you do, HSBC can cancel the reward.

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Why pick this card

4 mpd on contactless, travel & online spend. Up to 8 mpd for HSBC EGA customers (S$50K ADB).

Currently hold a HSBC credit card issued over 12 months ago? Apply here → HSBC gives eligible existing cardholders S$50 cashback directly. Please complete the Rewards Redemption Form sent to your email so your application is properly recorded.

If you cancelled a HSBC credit card in the past 12 months, you don't qualify for either reward.

ENDS 31 AUG 2026 · 22 DAYS LEFT

Direct (Citi)

40,000 Bonus Citi ThankYou Points

Requirements

- Eligible for new main Citi Cardmembers only (no existing Citi card, no Citi card closed in the past 12 months)

- Spend S$800 in the first 2 months of card approval

Valid till 30 Sep 2026

Via SingSaver

🎁 Choose 1 Gift

Dyson Airstrait™ Straightener

Retail S$799

Hair straightener that dries and smooths hair at the same time

25,000 Max Miles by Heymax

Worth S$600+

Earns you miles redeemable for flights, hotels, and perks

Dyson V8 Cyclone Vacuum Cleaner

Worth S$559

Cordless cleaning vacuum with strong suction

S$440 Grab Voucher

worth S$440

Use on Grab rides, GrabFood, GrabMart, and other Grab services.

S$400 Cash via PayNow

No bank details needed

Requirements

- You qualify if: you have no Citibank credit card right now AND haven't cancelled any Citi credit card in the last 12 months

- Spend min. S$500 within 30 days of card approval

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Valid till 31 Aug 2026

Why pick this card

4 mpd on any online transaction + offline fashion & department stores. No minimum spend.

Why pick this card

10X DBS Points (4 mpd) on all online spending (cap S$1,000/month).

Why pick this card

XL Rewards: 4 mpd · XL Cashback: 5% — on dining, travel, shopping, and foreign currency spend.

Why pick this card

10X UNI$ (4 mpd) on contactless mobile wallet + online shopping/entertainment.

ENDS 31 AUG 2026 · 22 DAYS LEFT

🎁 Choose 1 Gift

Selection form emailed after application

S$95 Cash

worth S$95

via PayNow

💡 The first 3 eligible applicants at 2PM daily will get S$400 Cash via Paynow or Dyson Airstrait Straightener worth S$799

Valid till 31 Aug 2026

Requirements

- You qualify if: you have no UOB credit card right now, AND haven't cancelled any UOB credit card in the last 12 months

- Spend min. S$500 within the first 30 days from card approval

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Why pick this card

Up to 3 KrisFlyer miles per S$1 on SIA/Scoot/KrisShop.

Why pick this card

Up to 3.33% cash rebate. Tiered minimum spend: S$300 / $1,000 / $2,000 monthly for higher rates.

ENDS 31 AUG 2026 · 22 DAYS LEFT

🎁 Choose 1 Gift

Selection form emailed after application

S$95 Cash

worth S$95

via PayNow

💡 The first 3 eligible applicants at 2PM daily will get S$400 Cash via Paynow or Dyson Airstrait Straightener worth S$799

Valid till 31 Aug 2026

Requirements

- You qualify if: you have no UOB credit card right now, AND haven't cancelled any UOB credit card in the last 12 months

- Spend min. S$500 within the first 30 days from card approval

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Why pick this card

No FX fees + up to 10% cashback on online/mobile spend + gym, telco & streaming (S$800 min). Pairs with UOB One Account.

Why pick this card

Up to 8% cashback on 5 chosen categories (from 10 options).

Requirements

- You qualify if: you have no DBS/POSB credit card right now, AND haven't cancelled any DBS/POSB credit card in the last 12 months

- Enter promo code SINGSAVER during application

- Spend min. S$500 within 30 days of card approval

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Why pick this card

6% cashback on shopping and public transportation (S$800 min spend).

ENDS 31 AUG 2026 · 22 DAYS LEFT

Direct (Citi)

S$300 Cash Back

Requirements

- Eligible for new main Citi Cardmembers only (no existing Citi card, no Citi card closed in the past 12 months)

- Spend S$800 in the first 2 months of card approval

Valid till 30 Sep 2026

Via SingSaver

🎁 Choose 1 Gift

Dyson Airstrait™ Straightener

Retail S$799

Hair straightener that dries and smooths hair at the same time

25,000 Max Miles by Heymax

Worth S$600+

Earns you miles redeemable for flights, hotels, and perks

Dyson V8 Cyclone Vacuum Cleaner

Worth S$559

Cordless cleaning vacuum with strong suction

S$470 Grab Voucher

Worth S$470

Use on Grab rides, GrabFood, GrabMart, and other Grab services.

S$430 Cash via PayNow

No bank details needed

Requirements

- You qualify if: you have no Citibank credit card right now AND haven't cancelled any Citi credit card in the last 12 months

- Spend min. S$500 within 30 days of card approval

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Valid till 31 Aug 2026

Why pick this card

5% cashback on big online purchases (up to S$12,000/year). No monthly cap.

ENDS 31 AUG 2026 · 22 DAYS LEFT

🎁 Choose 1 Gift

Selection form emailed after application

S$95 Cash

worth S$95

via PayNow

💡 The first 3 eligible applicants at 2PM daily will get S$400 Cash via Paynow or Dyson Airstrait Straightener worth S$799

Valid till 31 Aug 2026

Requirements

- You qualify if: you have no UOB credit card right now, AND haven't cancelled any UOB credit card in the last 12 months

- Spend min. S$500 within the first 30 days from card approval

- SingSaver will email you a Rewards Redemption Form — check inbox (and spam folder) after applying. Fill it in within 14 days to claim your gift, or you'll lose it.

Why pick this card

3.33% base cashback + up to 6.67% bonus on Grab, Shopee, SP Utilities, McD & SimplyGo. Requires consecutive monthly spend.