Credit cards are incredibly convenient — but they can also become expensive very quickly if you miss a payment.

A single late payment can trigger:

- Late fees

- Finance charges

- Interest on new purchases

- Possible overlimit fees

- Negative impact on your credit profile (if prolonged) — repeated late payments or carrying high balances can lower your credit score, which affects your ability to get loans, mortgages, or other credit in the future.

The good news? Some of these charges are negotiable if they are not frequent (within reasonable doubt, for example: you forgot).

This ultimate guide will show you how to reduce or eliminate late fees and interest charges, step by step. But first let’s define:

What Are Credit Card Late Fees?

If you fail to pay at least the minimum amount due by your statement’s payment due date, most banks will impose a late payment fee of S$100 or depending on the bank and card type. But what many cardholders don’t realise is how strict and automated this process is.

1. The System Is Automated — Not Manual

Late fees are usually system-generated.

Here’s what happens behind the scenes:

- Your statement is issued.

- A due date is set (usually 20–25 days later).

- If the bank’s system does not detect the minimum payment received by the cut-off timestamp, it auto-triggers:

- Late payment fee

- Finance charges (if applicable)

- Possible suspension of interest-free period

There is typically no grace period, even if you’re only slightly late.

2. Being 1–2 Days Late Still Counts

Many people assume: “If I pay the next day, it should be fine.”

Unfortunately, that’s not how it works.

Banks usually define “on time” as:

- Payment successfully received and processed

- Before the exact due date cut-off (sometimes by 5pm or end-of-day processing time)

If your payment is reflected on the system after the due date, even by one day, the late fee is triggered.

This includes:

- Paying via FAST at night after the processing window

- Transferring funds on the due date but it reflects the next day

- Weekends or public holiday delays

3. GIRO Failures Still Trigger Late Fees

Even if you’ve set up GIRO auto-debit, you are still responsible for ensuring sufficient funds.

Common situations:

- Your salary hasn’t been credited yet

- Another deduction happened first

- You forgot about an earlier transaction

- Your bank account had insufficient balance

If GIRO fails, the bank’s system records it as non-payment, and the late fee applies automatically. GIRO setup does not guarantee protection from late fees.

What Are Finance (Interest) Charges?

When you don’t pay your full statement balance by the due date, your bank starts charging finance charges (interest) on the unpaid amount.

Most credit cards charge around:

- 26%–28% per annum

- Calculated on a daily compounding basis

That headline number alone is already high. But the way it’s calculated is what makes it expensive.

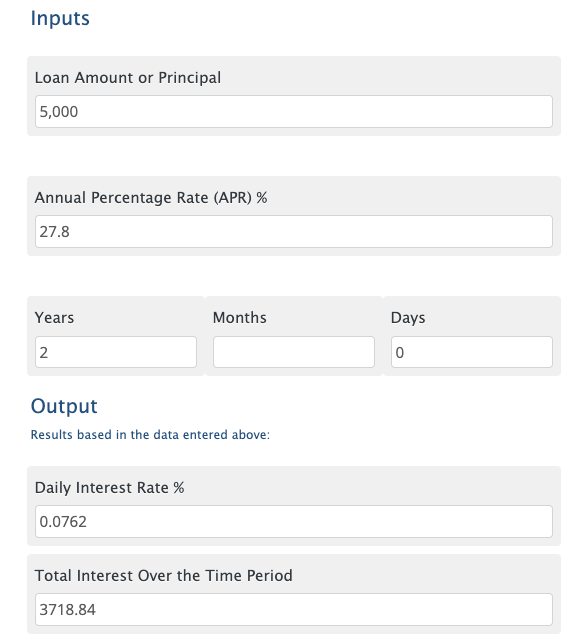

1. It’s 26%–28% p.a. — But Charged Daily

The advertised rate (e.g. 27.8% p.a.) is an annual rate, but the bank doesn’t wait a year to apply it.

Instead:

- The annual rate is divided into a daily interest rate

- Interest is calculated every single day

- It is applied to your outstanding balance daily

- The next day’s interest is calculated on the new higher balance

2. Interest Applies to More Than You Think

When you don’t pay in full, interest may apply to:

- The unpaid statement balance

- New retail transactions (with no grace period)

- Late fees

- Overlimit fees

If you had S$3,000 outstanding overdues last month and made another S$1,000 in new purchases this month, interest may apply to the full S$4,000 immediately.

3. Minimum Payment Is Not Protection

Paying the minimum amount due avoids late payment fees nut does NOT avoid interest charges, only the late payment fee.

Minimum payments are usually around:

- 3% of outstanding balance, or

- S$50, whichever is higher

If you owe S$5,000 and only pay the minimum, the remaining balance continues accruing interest daily at 26%–28% p.a.

At that rate:

- Interest alone can exceed hundreds of dollars over time.

- It can take years to fully clear the debt.

Now that you understand how late fees and finance charges work — and why they can escalate so quickly — let’s break it down by bank. While most credit cards in Singapore follow similar principles, each bank has its own terms, internal policies, and waiver tendencies. Below, we’ll look at the individual bank fees and the typical process to successfully request a late fee or interest charge reversal.

Table of Late Payment Fees and Finance Charge

Bank | Late Payment Fee | Minimum Monthly Payment | Finance Charge |

Citibank | S$100 | 1% (or S$50, whichever is greater) | Standard Rate: 27.9% p.a. Promotional Rate: 21.9% p.a., may be extended for good account conduct Penalty Rate: 30.9% p.a. if account is past due |

SC | S$100 | 1% (or S$50, whichever is greater) | 27.9% p.a.; 0.076% daily on outstanding balance until full payment |

HSBC | S$100 | 3% (or S$50, whichever is greater) | 27.8% p.a. |

DBS/POSB | S$100 | 3% (or S$50, whichever is greater) | 27.8% p.a. |

UOB | S$100 | 3% (or S$50, whichever is greater) | 27.8% p.a. |

OCBC | S$100 | 3% (or S$50, whichever is greater) | 27.78% p.a. |

CIMB | S$100 | 3% (or S$50, whichever is greater) | 27.78% p.a. |

DCS | S$100 | 5% (or S$50, whichever is greater) | 27.78% p.a. |

How to Request for Late Fee/Finance Charge Reversal:

Via Phone

- Call +65 6225 5225 using the mobile number registered with Citibank.

- Press 1 for credit card and bank account–related enquiries.

- Enter your NRIC number (numeric digits only) or the last 4 digits of your card number.

- Press 1 to request a late fee and interest charge waiver.

- The automated phone banking system will address you by your last name for verification.

- You’ll receive an SMS once your fee waiver request has been approved.

Alternative option:

You may also log in to Citibank Online and send a secure message to request a fee waiver.

Via SC Mobile/Online Banking

Step 1: Go to Help & Services. Under Service request by category, select Card Management, then choose Credit Card Fee Waiver.

Step 2: Pick the type of fee. You’ll then see the cards that are eligible for a waiver.

Step 3: Select up to five (5) cards, then click Next.

Step 4: Review and agree to the Terms & Conditions, then click Yes.

Step 5: The eligible fee transactions will be displayed.

Step 6: Choose the specific transactions you’d like to request for waiver.

Step 7: Review the request details on the confirmation page.

Step 8: You’ll see an acknowledgement screen confirming your submission.

Via Phone

- Call Standard Chartered’s Phone Banking hotline.

- Listen to the menu prompts.

- Press 2 for Fee Waivers.

- Press 2 again for Credit Card Late Fee Waiver.

- Enter your 16-digit credit card number.

Notes:

- Approval of the waiver is at the Bank’s discretion.

- You may submit for finance charge waiver via phone, live chat, and any branches only

Via Phone is the only way to apply for a fee waiver

- Dial 1800-HSBC-NOW (1800-4722-669).

- Select 8 for credit card fee waiver.

- Choose 2 for late payment fee waiver or 3 for finance charge fee waiver.

- Key in your 16-digit credit card number when prompted.

Once your waiver request is approved, you will receive an SMS from HSBC-RETAIL within two weeks. The fee reversal will be reflected in your next credit card statement.

For DBS/POSB credit cards, late fee and finance charge waivers are generally processed through their automated channels, rather than manual officer requests.

Key Things to Note:

- Fee waiver requests are handled via the automated system.

- Phone Banking fee waiver service is unavailable daily from 2:30am to 2:45am (system maintenance window).

- Fee waiver requests via DBS digibot are available 24/7.

- You will receive an email or SMS notification within 3 working days informing you of the outcome (based on your registered contact details).

How to Request a Waiver via DBS digibot

Step 1: Log in to DBS/POSB digibank (app or website)

Step 2: Click on the red digibot icon

Step 3: Type “Fee Waiver” in the chat

Step 4: Tap Fee Waiver, then select Authenticate me

Step 5: Complete authentication via iBanking login or Card & PIN

Step 6: Select Credit Card Fee Waiver

Step 7: Choose the type of fee you want waived (e.g. late fee or finance charge)

Step 8: Select the credit card account

Step 9: Review the details and tap Confirm

Via Phone:

- Dial 1800 111 1111 (within Singapore)

- Dial +65 6327 2265 (from overseas)

Then follow these steps:

- Press 1 for English (or 2 for Mandarin).

- Hold the line until prompted to enter your NRIC / Debit Card number / Credit Card number.

- If your mobile number is registered with the bank, you will receive an SMS OTP for authentication.

- Press 1 for Fee Waiver Request.

- Press 1 again for Credit Card Fee Waiver.

Once submitted, the system will assess your eligibility based on your account history and internal criteria.

Fee waiver requests for UOB Credit or Debit Cards are now only accepted via automated self-service channels. Requests through customer service officers are no longer available.

You can submit a fee waiver request using any of the following channels:

1. UOB TMRW App

- Log in and go to Accounts.

- Select your card.

- Tap Waive Fees.

- Choose the fee you want to waive and click Next.

- Review your request and confirm.

- See the waiver outcome instantly.

2. Phone Banking

- Dial 1800 222 2121.

- Press 1 for English or 2 for Mandarin.

- Press 1 for UOB chat services & phone banking.

- Press 2 for Fee Waiver & Application Status.

- Press 1 for Credit Card Fee Waiver.

- Press 2 for Finance Charge or Late Fee requests.

3. UOB Digital Assistant

- Visit UOB Digital Assistant and click the chat icon.

- Complete the security check.

- Agree to the terms & conditions and select Continue.

- Tap Fee Waiver, then select Credit Card.

- Choose the fee you want to waive.

- Enter your card number and click Submit to proceed.

Step 1: Log in using your access code & PIN, OCBC OneLook™, or OCBC OneTouch.

Step 2: Go to “More” → Card Services → Request Fee Waiver / Request Credit Card Fee Waiver.

Step 3: Select the card you want the waiver for and submit your request.

Step 4: Done! Your request is submitted.

Step 1: Select your card in the Card Management section and tap “To Manage”.

Step 2: Tap “Request Fee Waiver”, choose the type of fee, and tap “Confirm”.

Step 3: You’ll receive a notification of the waiver status within 5 days. You can also check the status anytime under “Waiver History” for that card.

CIMB has not publicly disclosed any procedures for waiving late fees or finance charges, but you can try requesting assistance through their phone support at +65 6333 6666

Best Practices When Requesting Waivers

1. Timing Matters

When requesting a fee waiver, timing is key — many banks allow one goodwill waiver if it’s not monthly recurrence, so it’s best to make the request soon after the charge posts. Banks respond more favorably to customers with consistent repayment records.

2. Explain & Appeal

When explaining the situation, provide context for the late payment, such as an emergency, a first-time oversight, or prompt repayment shortly after the due date. If your initial request is denied, don’t hesitate to ask to speak with a supervisor or escalate the matter.

3. Leverage Your Relationship

Emphasize your long-term relationship, spending habits, and potential future business, as banks are more receptive to loyal customers. I’ve never had to use this though.

4. Fallback & Record-Keeping

As a fallback, if a waiver is refused, consider closing the card before the next annual fee is applied. Finally, keep thorough records of all communications, as they can be invaluable for follow-ups or future disputes.

Proven Methods to Prevent Credit Card Late Fees/Finance Charges:

1. Set Up Automated Payments

To make timely full payments easier, enrol in automated payment plans with your bank. Most Singapore banks, including DBS, OCBC, UOB, and Citibank, let you auto-debit either the full balance or minimum payment each month. Auto-pay ensures you never miss a due date, even during busy months.

2. Enable Due Date Notifications

Activate SMS or app notifications for upcoming payments. Many banks offer reminders ranging from a week before the due date to a day-before alert, which can be combined with calendar apps for extra assurance.

3. Pay in Full and On Time — The Most Important Strategy

The single most effective way to avoid credit card late fees and finance charge is simple: always pay your full balance by the due date. Paying only the minimum can quickly lead to mounting interest charges, while missing the due date can trigger fees. Settling your balance in full not only keeps you fee-free, but also protects your credit score and allows you to fully enjoy your card’s rewards and benefits. No other strategy is as reliable or impactful as this — think of it as the foundation of responsible credit card use.

What To Do If Late Interest Fees Have Already Been Snowballing?

Watch this video where I have shared a method to reduce the interest charges. Alternatively, approach Credit Counselling Singapore to get help with debt consolidation.

Conclusion

Credit cards offer incredible convenience, but they can quickly become costly if payments are missed or balances are carried forward. While fee and interest waivers are sometimes possible, the most reliable and stress-free way to avoid late fees, finance charges, and potential credit score impacts is clear: pay your full balance on time. Setting up automated payments, enabling reminders, and monitoring your account are helpful tools, but they all support the same goal — staying in control of your credit and keeping it cost-free. Paying in full and on time is not just a best practice — it’s the single most effective strategy to protect your finances and maximize the benefits of your credit cards.